According to the latest report from market research firm Cignal AI, the shipment forecast for 800G ZR/ZR+ pluggable coherent modules has been significantly increased to over 200,000 units by 2026. 800ZR/ZR+ is rapidly becoming a key enabler for high-speed interconnection between next-generation AI data centers.

The I era is driving accelerated demand for 800G ZR/ZR+. As AI models scale, computing systems face dual bottlenecks in space and energy consumption. Distributed AI cluster deployment is becoming a trend, and the demand for high-speed connectivity between data centers is rapidly increasing.

Hyperscale data center cloud service providers, such as Meta, are adopting 800G ZR/ZR+ modules to connect geographically dispersed data centers via IP-over-DWDM. The power and performance of Gen120C optical modules enable long-distance 400G and 800G coherent transmission, with performance comparable to traditional on-board solutions.

Most major hyperscale data center operators will use 800ZR/ZR+ modules for a portion of their capacity. Even those planning to skip 800G and move directly to 1.6T, such as Microsoft, are evaluating 400G Gen120C modules (also known as 400G-ULH).

Scott Wilkinson, Chief Analyst at Cignal AI, said:

“The new forecast reflects an accelerating shift in how hyperscale data centers deploy high-performance optical components. The demand for high-bandwidth, long-distance connections between AI clusters is accelerating the deployment of 800G ZR+. Pluggable 800G coherent modules, with comparable performance to onboard solutions, are gradually eroding the market share of other coherent optical modules.”

The success of 400G ZR reveals how 800G ZR can be rapidly implemented. 400G ZR/ZR+ is the first coherent optical technology to be widely used in data communications. Its commercial shipments are more than three times that of other coherent technologies during the same period. Its success also provides important insights for 800G ZR/ZR+:

Key to success: Consistent with router port speed (400G) QSFP-DD/OSFP package enables router compatibility with data center applications Decoupled multi-vendor ecosystem (promoting interoperability and economies of scale) Direct inspiration: For 800G ZR/ZR+ to be rapidly implemented, it is necessary to focus on standardized packaging, clarify application scenarios, and promote standardization.

800ZR/ZR+: Application Targets and Market Opportunities

Application Scenario Segmentation

Metro Data Center Interconnect (DCI): 800G ZR+ is suitable for AI cluster connections over hundreds of kilometers.

400G-LH (Gen120): Leveraging coherent modulation to cover longer distances, with primary demand concentrated in the Chinese market.

800G ZR+: Thanks to the interoperable PCS standard, it has become the mainstream choice, with leading customers such as Meta achieving large-scale deployments.

400G Interoperability Mode: Targeting certain transition scenarios and meeting forward compatibility requirements.

Market Drivers

Major DSP and Module Vendors: Cisco/Acacia, Ciena, Infinera, Nokia, ZTE, etc.

Key Customers:

Meta: Early deployment, driving the commercialization of 800ZR+

Google/AWS/Oracle: Later deployment

Microsoft: Skipping 800G but prioritizing 400G ULH and future 1.6T ZR deployments

Market Size and Trend Forecast

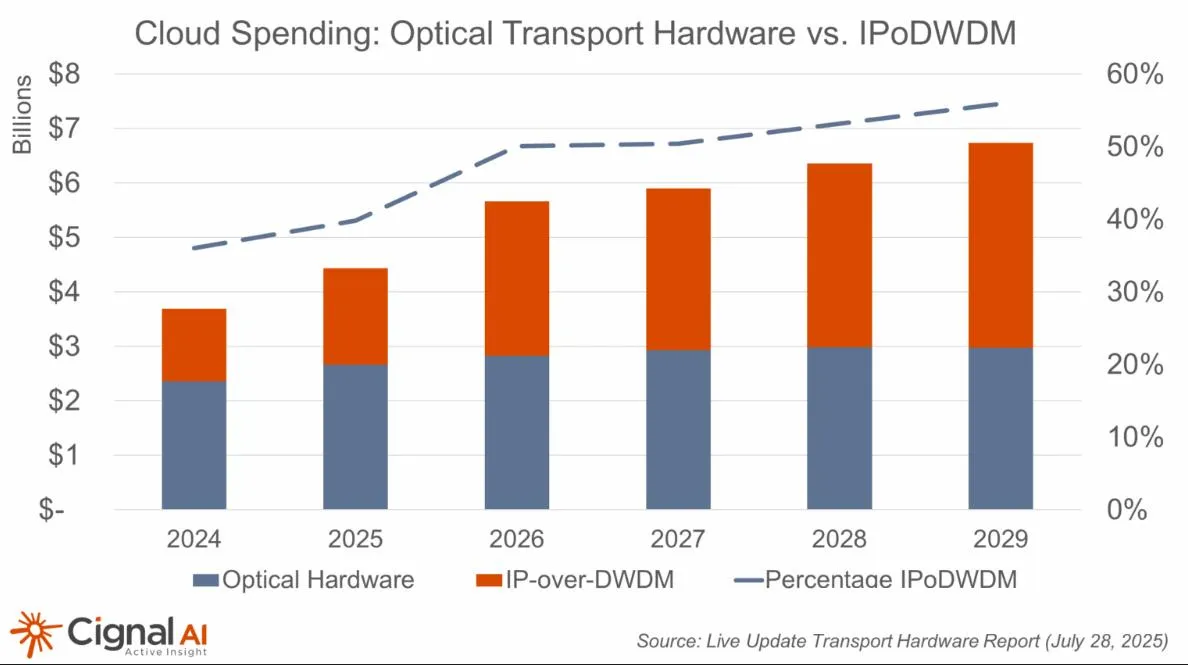

Market Size: Pluggable coherent optical modules are key to the transition to IP-over-DWDM networks. Routers and switches directly carry DWDM optical components. This architecture generated a $2 billion market in 2025 and is expected to reach nearly $5 billion by 2029.

Main Deployment Force: Over 80% of deployments are expected to come from cloud service providers, and the IP-over-DWDM architecture will completely replace traditional optical transmission equipment.

Product Replacement: The rise of 800G ZR+ will squeeze the market for onboard 800G and 1.2T+ modules. 05—Summary: 800G ZR/ZR+ is not merely a continuation of 400G ZR/ZR+, but rather a key driver of the optical network architecture transformation in the AI era. Its pluggable, programmable, long-distance, and high-performance features make it a core component of the IP-over-DWDM architecture. Over the next three years, industry chain collaboration will become the primary battlefield for high-value competition.

Market Size and Trend Forecast

Market Size: Pluggable coherent optical modules are key to the transition to IP-over-DWDM networks. Routers and switches directly carry DWDM optical components. This architecture generated a $2 billion market in 2025 and is expected to reach nearly $5 billion by 2029.

Main Deployment Force: Over 80% of deployments are expected to come from cloud service providers, and the IP-over-DWDM architecture will completely replace traditional optical transmission equipment.

Product Replacement: The rise of 800G ZR+ will squeeze the market for onboard 800G and 1.2T+ modules.

Summary

800G ZR/ZR+ is not merely a continuation of 400G ZR/ZR+, but rather a key driver of the optical network architecture transformation in the AI era. Its pluggable, programmable, long-distance, and high-performance features make it a core component of the IP-over-DWDM architecture. Over the next three years, industry chain collaboration will become the primary battleground for high-value competition.