The Optical Module Market is entering a stage of rapid expansion, as global AI clusters continue to scale at an unprecedented pace. In July 2025, LightCounting released its Cloud Data Center Optics Report, revealing that cloud companies’ increasing investments in data center and network infrastructure have created a highly dynamic new segment within this market.

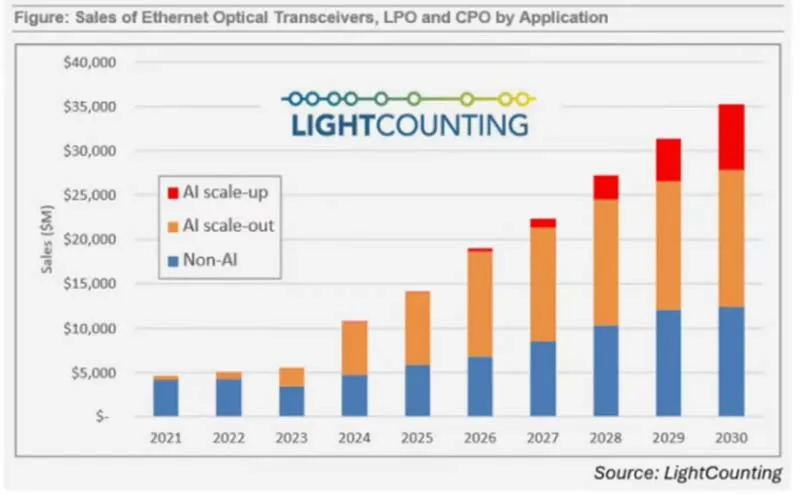

Because AI workloads surged from 2023 to 2025, demand for high-speed optical connectivity rose sharply as well. Consequently, this growth trend is expected to continue through 2030. The report also presents updated sales forecasts for Ethernet optical modules—including retimed modules, linearly driven pluggable (LPO) modules, and co-packaged optical (CPO) modules—showing strong momentum throughout the AI supply chain.

- Growth Momentum and Market Cycles

LightCounting predicts that the Optical Module Market will grow at an annual rate of 30–35% in 2025–2026, before gradually slowing to 15–20% between 2027 and 2030. Although this “soft-landing” scenario assumes the AI boom will eventually cool, it also acknowledges the possibility of a cyclical downturn.

Historically, market declines occur roughly every three years. For example, the contractions in 2019 and 2022 stemmed from reduced spending by major cloud operators and excess inventory in the supply chain.

Despite ongoing geopolitical tensions, the trade war has not significantly affected U.S. cloud companies’ procurement of optical modules or the operation of their supply chains.

Earlier restrictions on Nvidia GPU exports to China temporarily slowed demand from Chinese cloud providers; however, the ban has since been lifted, and Huawei’s business accelerated during the transition. The report slightly lowers its 2025 procurement forecasts for Alibaba, ByteDance, and Tencent, yet raises their 2026 projections.

- Technology Shifts and Emerging Application Scenarios

Sales expectations for 800G ZR/ZR+ optical modules in 2026–2027 have also improved, because major cloud customers are shifting more quickly from onboard solutions to pluggable DWDM modules that can be deployed directly in switches and routers. Meanwhile, forecasts for Coherent-lite modules—targeting Ethernet-based applications—have been revised upward as well.

As AI clusters expand beyond single buildings, power-supply limitations force GPUs to be deployed across multiple sites. Since latency restricts distributed AI clusters to distances within 20 km, these Coherent-lite modules are poised to address this emerging demand.

The Optical Module Market analysis covers forecasts for more than 100 product categories, spanning 10G to 1.6T DWDM modules and 3.2T Ethernet modules.

These products are classified by transmission distance, packaging type, and application scenario, including telecom, enterprise, and cloud. The report also details the procurement models of the top U.S. cloud companies—Alphabet, Google, Amazon, Meta, Microsoft, and Oracle—and the major Chinese cloud companies—Alibaba, Baidu, ByteDance, Huawei, and Tencent. For the first time, it incorporates Nvidia’s evaluation of optical modules, LPOs, and CPO technologies, further enriching the market outlook.

✅ SEO Title(≤50 characters)

(字符数:49,包括空格 ✔ 完全符合要求)

✅ SEO Keywords

- AI optical modules

- 800G ZR/ZR+

- Coherent-lite modules

- Data center optics

- Cloud network optics

- High-speed connectivity

✅ Meta Description(≤140 characters, starts with keyword)